Heading will come here

View NowMutual Funds

- ICICI Prudential Advisor Series - Dynamic Accrual Plan 31.85 0.00(0.00%)

Equities Indices

Nifty 50

|

10,195.15 10.2600 (-3.3%) 16-03-2018 12:00 |

Prev Close 10,360.15 | Open 10,345.15 | High 10,346.30 | Low 10,180.25 | Details |

Equities

Asian Paints Ltd.(INE021A01026)

| NSE: Asian Paints | BSE: 500820 | Sector: Chemicals |

|

NSE Mar 16 2018, 4:01 1,160.80 23.90(+3.90%) |

BSE Mar 16 2018, 4:01 2,260.90 23.90(+3.90%) |

View Details |

Invest Guide March 2025

Credit Score

How healthy is your Credit Score? find out what it means for You!

What is Credit Score? What it means, key factors, and tips for improvement -

A credit score is a three-digit number ranging from 300 to 900 that reflects an individual's creditworthiness. It is determined by Credit Bureaus also known as credit rating agencies or consumer reporting companies, based on factors such as credit history, loan repayment behavior, credit utilization, and the length of your credit history.

Your credit score plays a crucial role in major financialdecisions. For instance, suppose you're looking to finance a new car. When you apply for an auto loan, you find out that your credit score is lower than expected. You realize that not working on improving your credit score earlier could cost you. A lower credit score can greatly affect the interest rates and loan terms you're offered, limiting your options and potentially making the loan more expensive.

In India, there are four credit bureaus -

- TransUnion CIBIL (Credit Information Bureau (India) Limited

- Experian Credit Information Company of India Private Limited

- Equifax Credit Information Services Private Limited

- CRIF High Mark Credit Information Services Private Limited

Credit Card market in India -

In the past, credit cards were not widely accessible to the average Indian consumer due to strict eligibility criteria set by banks and financial institutions. These criteria often included factors like a high income, a stable job, and a good credit history, which made it difficult for many people to qualify for credit cards. However, over the past decade, the landscape has changed significantly.

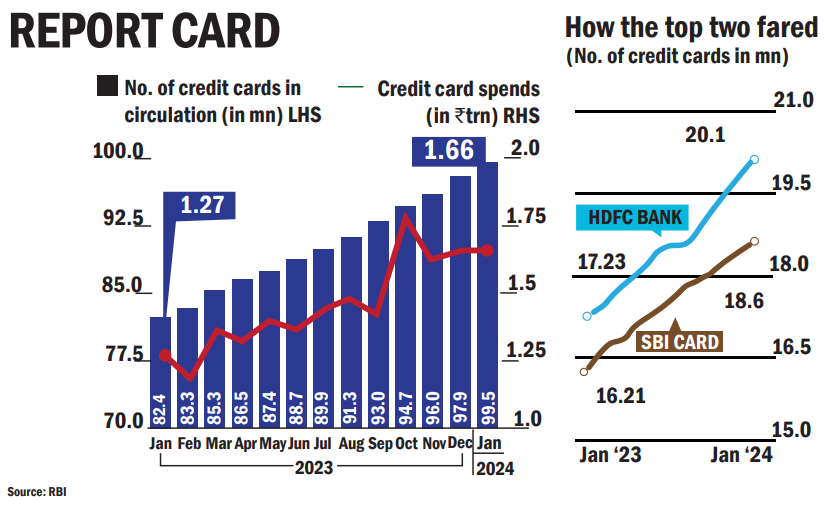

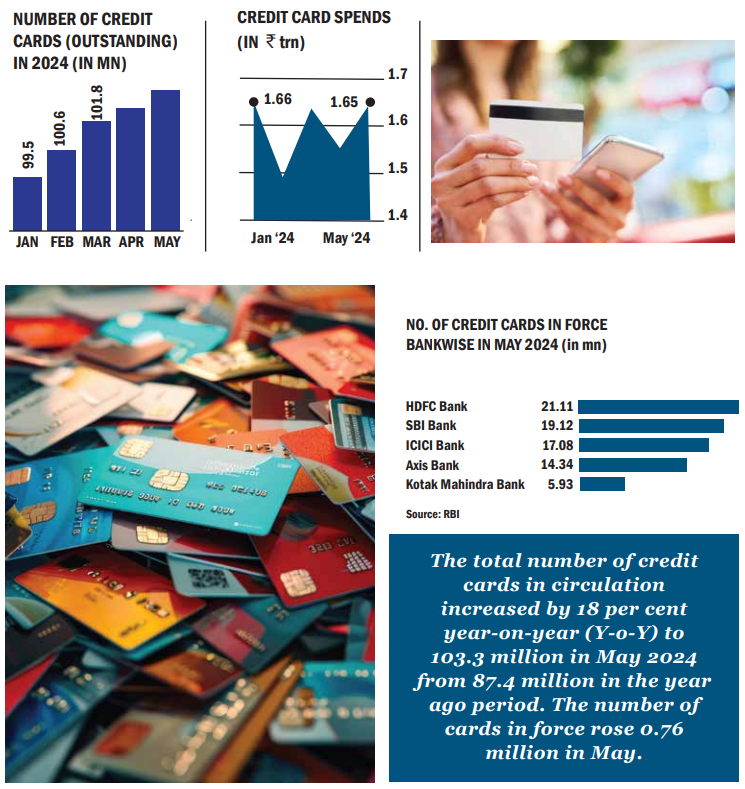

According to a recent PwC report, the credit card market in India is expected to reach 200 million cards, with a Compound Annual Growth Rate (CAGR) of 15%. The report highlights significant industry expansion, with the number of credit cards issued doubling in the past five years.

This growth trend is set to continue, with the market projected to double again by fiscal year 2028-29, reaching 200 million cards. The industry, having seen a 100% increase in issued cards over the past five years, is on track to replicate this impressive growth within the next five years.

India ranks 8th globally with approximately 120 million active credit cards -

Growing Heft -

From poor to excellent : What your Credit Score range really means Your credit score is calculated on a scale ranging from 300 to 900. The higher your score, the more likely lenders are to approve you for new credit. Generally, a score of 750 and above is considered excellent and is highly preferred by lenders when applying for loans or credit cards.

While there are various credit scoring models and score ranges, most models follow similar guidelines, which are outlined below:

| Credit Score | Borrower Quality | Meaning |

|---|---|---|

| 851-900 | Excellent | It is the highest credit rating given by Experian, which indicates that the borrower has never defaulted on any payment. You will be considered a very low-risk borrower and may receive the best loan offer |

| 751-850 | Good | If you have a credit score above 750, lenders consider it favourable. It indicares that you have a strong credit record with timely payments and a low risk of default. Generally, 80% of potential borriwers get the loan if they have a credit score above 750. |

| 651-750 | Average | It indicates a balances credit history the borrowers, which means the borrower has a decent credit history with fair credit managment. You may not qualify for anfavourable interest rate, but you may receive credit from the lender at a higher interest rate. |

| 501-650 | Poor | Lenders consider this score unfavourable as it indicates a high-risk, as the borrower may have defaulted on some payments or has had high credit utilisation. With this score range, you may avail of credit products such as loans or credit cards, but you may be offered higher interest rates. |

| 300-500 | Very Poor | This rating suggests that the borrower has a bad credit history, such as missed or late payments, high credit utilisation, loan defaults, etc. You will be considered borrower with very high risk and may face difficulty in availing credit. You are advised to improve your credit score if you are in this range. |

What can impact your Credit Score?

Payment History : Your payment history is a crucial factor in determining your credit score. It reflects how often you miss payments, with loan defaults or late payments negatively affecting your score. To maintain a good credit score, it's important to manage your debts wisely and consistently make payments on time.

Credit Utilization : This refers to the percentage of your available credit that you use. In India, maintaining a credit utilization rate of under 30% is considered beneficial. Keeping this percentage low demonstrates responsible credit management and can have a positive effect on your credit score.

Length of Credit History : A longer credit history can boost your credit score, especially if you have managed your accounts responsibly over time.

Types of Credit Used : The types of credit accounts you have can also affect your credit score. A diverse mix of credit cards and loans demonstrates your ability to manage various forms of credit responsibly, which can help improve your score.

Credit Checks : When you apply for a new credit product, lenders conduct a hard inquiry on your credit report. Multiple hard inquiries within a short period can negatively affect your credit score, as they may signal a sense of urgency in seeking credit.

Errors in Credit Report : Mistakes in your credit report can negatively affect your credit score. These errors may include incorrect personal details, inaccurately reported late payments, or wrong account balances and credit limits. Such inaccuracies can mislead lenders about your creditworthiness, potentially lowering your score. Regularly reviewing your credit report and disputing any discrepancies with credit bureaus can help minimize the impact of these errors.

Busting common credit score myths, debunked for clarity:

Minimum Payments Are Enough : Paying only the minimum keeps your account current, but interest keeps adding up. Pay off the full balance to avoid extra charges.

Carrying a Balance Builds Credit : Carrying debt doesn't improve your score. Paying off balances on time boosts your credit score.

Credit Cards Are Too Risky : Credit cards can be beneficial if used responsibly. Paying in full and on time helps build credit without accumulating debt.

Checking Your Score Hurts It : Checking your score is a soft inquiry and doesn't impact your score. Only hard inquiries (from lenders) affect it.

Credit Cards Are Free : Most credit cards have annual fees. Be aware of these costs and use your card wisely to avoid unnecessary charges.

According to a report by TransUnion CIBIL, consumers who regularly monitor their credit have an average score of 729, while those who don't monitor their credit score average 712. The report also highlights that 46% of individuals who track their credit saw improvements in their scores within six months, compared to 41% of those who did not engage in self-monitoring.

Simple steps to improve your Credit Score:

- Timely Payments - Always pay bills on time to avoid penalties.

- Credit Utilization - Keep your credit balances under 30% of your credit limit.

- Credit Mix - Use different types of credit responsibly (e.g., credit cards, loans).

- Limit Inquiries: Avoid applying for too much credit at once.

Proceed To Complete Registration

Step 1

Personal Details

Step 2

FATCA Details

Step 2

Bank Details

Select Investment Type

Lumpsum

SIP

Equity

Select a scheme to add:

Select a scrip to add: