Heading will come here

View NowMutual Funds

- ICICI Prudential Advisor Series - Dynamic Accrual Plan 31.85 0.00(0.00%)

Equities Indices

Nifty 50

|

10,195.15 10.2600 (-3.3%) 16-03-2018 12:00 |

Prev Close 10,360.15 | Open 10,345.15 | High 10,346.30 | Low 10,180.25 | Details |

Equities

Asian Paints Ltd.(INE021A01026)

| NSE: Asian Paints | BSE: 500820 | Sector: Chemicals |

|

NSE Mar 16 2018, 4:01 1,160.80 23.90(+3.90%) |

BSE Mar 16 2018, 4:01 2,260.90 23.90(+3.90%) |

View Details |

Invest Guide November 2024

Cover Story: 10 Investments To Combat Inflation A Comprehensive Guide

Inflation is like a quiet thief, gradually leading to a loss of purchasing power. As prices go up over time, the money you have buys less. Inflation is a key economic concept that refers to the gradual increase in the price level of goods and services in an economy over time. Fighting inflation isn't just about keeping your current lifestyle, it's crucial for protecting your financial future.

A subject of concern and debate all over the world, inflation profoundly impacts your savings and investments and thereby compromising your financial future. In this context, understanding inflation and its impact on personal finances require careful management, wise investment strategies and decisions to mitigate the negative consequences.

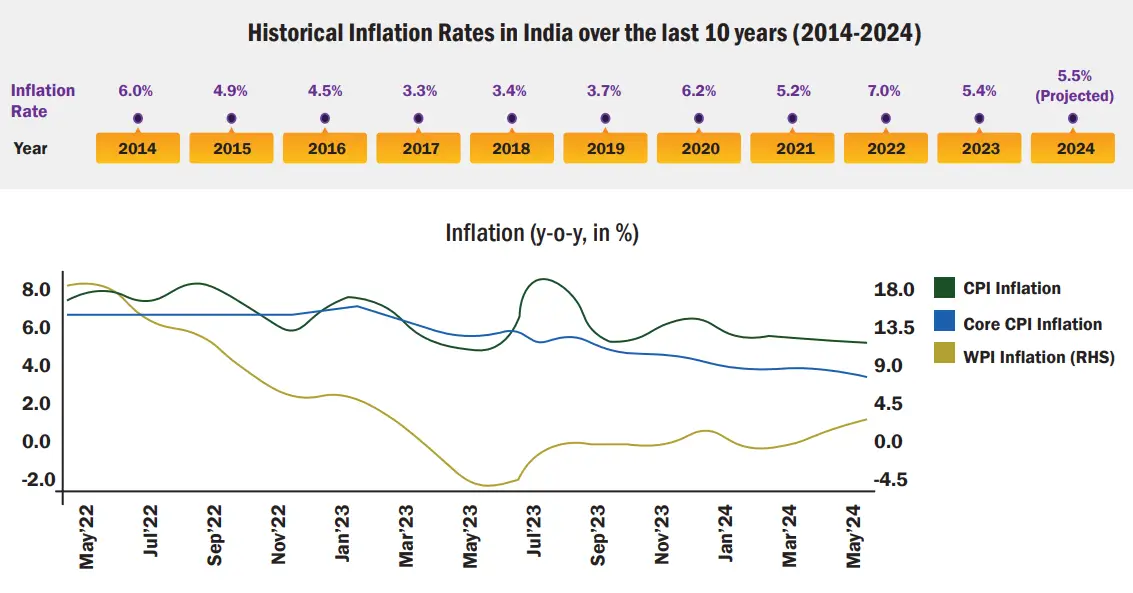

Inflation trends in India: Last 10 years -

Over the past decade India has experienced notable fluctuations in inflation rates influenced by various economic factors including rising food and fuel prices, supply chain disruptions caused by the Covid -19 pandemic and government policies. In India, the inflation rate is measured using two indices, the Consumer Price Index (CPI) and the wholesale price index (WPI).

The CPI tracks the change in the price of a basket of goods and services consumed by a household like food, clothing, household, transportation and healthcare. The WPI analyses the inflation of only goods across 697 commodities. WPI-based wholesale inflation considers the price change at which consumers buy goods at a wholesale price or in bulk from factories, mandis, etc.

Inflation poses challenges and impacts the Indian household in majorly two areas - necessities like food, clothing and healthcare and other category of expenditure like education, housing etc. both in terms of affordability and availability. To exemplify this, let us take the standard price of bread (400 gms) in the year 2021 was Rs25/ - Rs30/ - With the current food inflation rate of 5.6%, the price of bread rose to Rs45/- reflecting the ongoing inflation and rising production cost. The rate of inflation for education has been significantly higher at 10%. A private engineering institution that charged Rs 1 lakh per year in tuition fees in 2010 has increased its costs to Rs 3 lakhs per year in 2022.

This loop can have long-term effects on health and future chances, particularly for vulnerable people. A survey conducted in March 2023 found that 58 percent of respondents in India reported that rising inflation affected their ability to pay for basic necessities such as food, clothing, and healthcare. In contrast, 49 percent of respondents said they were unable to save because of inflation. Addressing these issues requires comprehensive policies focused on stabilizing prices as well as enhancing economic resilience with prudent investment strategies by individuals.

Here's a summary of the historical inflation rates in India over the past decade, primarily based on the Consumer Price Index (CPI):

Key Takeaways -

It is unknown whether the future will witness higher-for-longer inflation or we see inflation being tamed quickly and rates falling back to previous historic levels. What is certain, however, is that the sooner investors learn to adapt to the potential new economic scenario, the better off they will be.

Adding commodities and real estate investments to a well-diversified portfolio of stocks and bonds can help mitigate inflation risks. Commodities, such as precious metals, energy, and agricultural products, often have a positive correlation with inflation. When prices rise, the value of these assets typically increases as well, helping to preserve purchasing power. They also add a layer of diversification to your portfolio and reduce overall volatility.

There's not a one-size-fits-all answer! The optimal course of action will depend on your wealth and stage of life.

Beating inflation involves investing your money in a way that yields returns exceeding the current inflation rate. In an era where inflation can drastically reduce your purchasing power, protecting your wealth has become more critical than ever. As prices rise, traditional savings may be insufficient to support financial stability and growth. Therefore, adopting effective investment strategies are crucial for protecting your assets from inflationary pressures.

In 2024, Indian investors will have a wide range of assets to choose from, including equities, real estate, inflation-linked bonds, and commodities that not only preserve and grow your wealth, but also ensure you stay ahead of rising costs and secure your financial future.

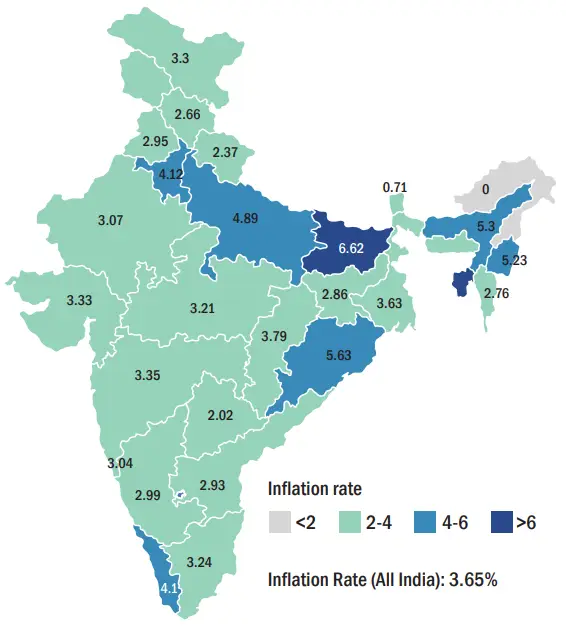

The below graph shows the State-wise inflation rates in India for August 2024(based on CPI) -

Statewise Inflation Rates (%) for August 2024 (based on CPI)

A few popular inflation - proof investment options that have proven effective in protecting investor's purchasing power over escalating prices are:

-

Gold -

Traditionally seen as a safe haven asset and a reliable hedge against inflation and a safe bet against market volatility, adding gold to your portfolio can help combat inflationary pressures. A globally accepted asset, gold is valued worldwide. While it may not provide regular income like stocks or bonds, its role as a store of value makes it a valuable component of a well-rounded investment strategy aimed at preserving wealth in an inflationary environment. -

Gold ETF & Sovereign Gold Bonds -

Besides jewelry and bullion gold investment you can choose to add gold to your investment in a non-physical form like Gold ETF and tax-free Sovereign Gold Bonds and eliminate the need to hold physical gold. Gold funds or Gold ETFs are mutual funds that invest in gold providing a more diversified approach to gold investing. Carrying the advantages of liquidity and diversification these funds are suitable for both seasoned and new investors. However, when deciding between gold funds and Gold ETFs as an investment option one must understand the fundamental differences in terms of liquidity, diversification and costs. You need a Demat and trading account to invest in gold ETFs whereas you can always invest in gold mutual funds either online or through an agent. -

Equities and Equity Mutual Funds -

Historically, equities have outperformed inflation over the long term. In contrast to traditional fixed deposit investments which offered only 7-8% interests, equity schemes of mutual funds gave a return of more than 14-15%. A rewarding asset class for long term investments equities have demonstrated steady returns in the past decade.

Equity investments into direct stock requires the investor to analyze stocks and make their own investments using a Demat (trading account).

Equity mutual funds collect money from investors and create an equity portfolio based on the scheme's goals. They eliminate the requirement for investors to do their own stock analysis and investment, which involves substantial expertise and experience. Equity mutual funds come under different categories like Mid-cap funds, Multi-cap Funds, Large Cap Funds and Flexi Cap funds, ELSS (Equity linked Savings Scheme) etc. Systematic Investment Plans (SIP) is a disciplined strategy for investors in the face of market volatility and inflation. By investing in mutual funds on a regular and consistent basis through SIPs, investors can benefit from rupee cost averaging and potentially obtain greater returns that outperform inflation. Further, the power of compounding is one of the most impressive aspects of SIP. Over time, this compounding effect can significantly enhance the value of one's portfolio.

-

Real Estate -

Real estate usually appreciates in value over time, and rental income typically rises alongside inflation, making it an excellent shield against rising prices. According to an analysis by sector consultancy Anarock, compared to inflation rates of 6.7% in 2022-23 and 5.4% in 2023-24, real estate prices have risen at a compound annual growth rate (CAGR) of 13%. Well-located properties in expanding markets retain their value and attract tenants even during economic downturns, offering a cushion against inflationary pressures. -

Real Estate Investment Trusts -

Investors who find it difficult to opt for real estate due to huge capital requirements can opt for REITs - an easier way to invest in real estate and diversify their portfolios and get the inflation hedging benefits of real estate. When inflation increases, property prices and rental income tend to rise as well. REITs typically thrive in inflationary environments since they can adjust rents upwards and distribute the resulting income to their shareholders. However, investors should evaluate the business model of a REIT before investing, as these entities can be affected by fluctuations in interest rates. -

Commodities (Non-Gold) -

Investing in commodities like energy, (oil, natural gas), and agricultural products (wheat, rice) have intrinsic value. As inflation rises, the cost of these physical goods tends to increase, preserving or enhancing their value. Their inherent value, diversification benefits, and price sensitivity to inflation make them appealing solutions for preserving wealth. ETFs (Exchange-traded funds) that track the price of specific commodities or a basket of commodities provide liquidity and ease of trading. -

Inflation Indexed Bonds and Debt Instruments -

If you're a low risk or risk averse investor, consider building a diversified portfolio with a larger exposure to debt-based assets like inflation indexed bonds and debt mutual funds. Instruments like the Government of India's inflation-indexed bonds (IIB) offer returns that adjust based on inflation, providing a safeguard for your capital. Though IIBs come across as a great tool as a hedge against inflationary markets, they carry the drawbacks of low yield and liquidity limitations making them less attractive to investors.

Investors who want to avoid market fluctuations of equity can also consider investing in debt-oriented mutual fund schemes. Debt funds can also help you to take advantage of investing in equity market along with safety on your principal amount through Systematic Transfer Plan (STP).

-

National Pension System (NPS) -

NPS invests in a mix of equities and fixed income, with potential for inflation-beating returns over the long term, making it suitable for retirement savings. Contributions to NPS are eligible for tax deductions under Section 80C (up to Rs 1.5 lakh) and an additional deduction under Section 80CCD(1B) (up to Rs50,000). The average return on equity-oriented NPS investments over the last 5 years have been between 15-20%. - Public Provident Fund (PPF) - A tax-advantaged Savings, PPF is a government-backed savings scheme that offers attractive interest rates, which can help protect against inflation while giving tax benefits. PPFs provide a fixed interest rate, which is reviewed and amended quarterly by the government. While the rate does not always surpass inflation, it has traditionally produced competitive returns, particularly during times of high inflation. The current PPF interest rate is 7.1% for Q3 of FY 2024-25.

-

Hybrid Mutual Funds -

Offering the advantages of diversification, these funds invest in a mix of equity and debt, balancing risk and return for the investor. They can provide better protection against inflation compared to pure debt instruments. Hybrid funds are managed by professionals who analyze market conditions and adjust portfolios accordingly, providing an advantage for investors who may not have the time or expertise to manage their investments actively. Most hybrid funds invest in equity and debt although there are funds that have more asset classes like gold, international equities, etc. in their portfolio.

According to AMFI data, SIPs per month have increased by 25% CAGR over the last seven years, reaching 19200 crore per month as of 29-Feb-24. Fund houses provide the option to begin SIPs with minimal amounts.

Disclaimer: Investments in securities markets are subject to market risks. Read all the related documents carefully before investing. The securities quoted are exemplary and are not recommendatory.

Proceed To Complete Registration

Step 1

Personal Details

Step 2

FATCA Details

Step 2

Bank Details

Select Investment Type

Lumpsum

SIP

Equity

Select a scheme to add:

Select a scrip to add: